Many Malaysian families assume their EPF savings or employer-provided insurance are enough. But if your income suddenly stops tomorrow, could your family maintain their lifestyle for the next 10–15 years?

There is no one-size-fits-all formula for life insurance in Malaysia, as the right coverage depends on income, debts, dependents, and financial goals. The primary purpose of life insurance is to provide financial protection for those who rely on you if you pass away.

Many people confuse it with medical coverage, savings plans, or investment policies, but life insurance is meant to replace income, not pay medical expenses.

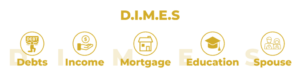

A practical and reliable way to estimate life insurance coverage is the D.I.M.E.S formula, adjusted to living costs and financial needs.

A practical and reliable way to estimate life insurance coverage is the D.I.M.E.S formula, adjusted to living costs and financial needs.

Why Life Insurance Is Important

Life insurance provides a death benefit to your family, ensuring they can maintain their lifestyle if your income stops. This benefit helps cover daily living expenses, such as food, utilities, transportation, and children’s education costs. The payout can be used to pay off outstanding debts such as home loans, mortgages, personal loans, and credit card bills to prevent your family from facing repayment burdens. It ensures your dependents — spouse, children, or parents — have financial stability even when you are no longer there to support them.The Quick Rule: 10–15x Annual Income

A good rule of thumb recommended by most advisors is to have life insurance coverage that is 10 to 15 times your annual income. For example, if your monthly income is RM5,000, your annual income would be RM60,000. Therefore, the suggested coverage amount would be between RM600,000 and RM900,000. This amount helps replace your income for your family in the event of something happening to you.A More Accurate Way to Calculate Coverage: The D.I.M.E.S Formula

A practical and reliable way to estimate life insurance coverage is the D.I.M.E.S formula, adjusted to living costs and financial needs.

D — Debts

This includes all outstanding financial obligations such as:- Housing loans

- Car loans

- Personal loans

- Credit card balances

I — Income Replacement

Ask yourself: How long would your family need financial support if your income stopped? A common Malaysian guideline:- Families with young children: about 15 years

- Families with older children: around 5–10 years

Inflation Adjustment

With Malaysia’s long-term inflation averaging 2–4%, RM1 million today could be worth only RM550k–RM670k in 20 years. That’s roughly a 33–45% drop in real terms. Education and living costs rise faster than general inflation, sometimes 5–8% annually, so your coverage needs to anticipate that trend. Look for policies with built-in inflation riders or automatic sum assured increases. Even with inflation riders, review your policy every 3–5 years to ensure coverage matches your goals and rising costs.E — Education Costs

Education is one of the largest future expenses for most families. Estimated costs include:- Local private university: RM80,000 – RM150,000 per child

- Overseas education: RM300,000 and above

S — Spouse Support

If your spouse depends on your income, additional protection should be considered, including:- Daily living expenses

- Medical and healthcare costs

- Long-term retirement support

- Savings and investments

- Existing life insurance policies

- Employees Provident Fund (EPF/KWSP) savings

- Death benefits from the Social Security Organisation (PERKESO/SOCSO)

Types of Life Insurance Available in Malaysia

- Term Life Insurance

- Whole Life Insurance

- Investment-Linked Policies (ILP)

- Mortgage Reducing Term Assurance (MRTA)

How Much Can You Afford?

Many Malaysians are underinsured because they believe that their EPF (Employees Provident Fund) savings or employer-provided insurance are sufficient. However, guidelines from Bank Negara Malaysia indicate that there are significant household protection gaps. This is because employer coverage typically amounts to only 1 to 2 years of income, which falls short of meeting family needs.Affordability Rule

Keep insurance premiums around 5–10% of your monthly income to ensure adequate protection without straining your budget. Example:- Monthly income: RM4,000

- Affordable premium range: RM200–RM400 per month

What Most People Need

For adequate coverage at a lower cost, term life insurance is the most affordable option. It is best suited for income protection and is ideal for young families. Investment-linked policies typically include medical coverage and savings components, but they are more expensive and may leave you underinsured if your budget is tight. Many financial planners recommend securing enough term coverage first, and then considering investment plans later.Underinsurance vs Over insurance

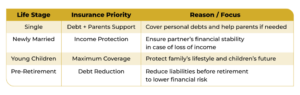

Being underinsured can leave your family vulnerable, sometimes forcing them to downgrade their lifestyle or even sell assets to cover unexpected costs. While being overinsured may create financial strain due to high premiums and increases the risk of a policy lapse if payments become unsustainable. Striking the right balance in insurance coverage is essential, ensuring adequate protection without overextending financially.Life Insurance Needs at Different Life Stages

When Should You Review Your Coverage?

Insurance needs evolve with life. Review your policies every 3–5 years or sooner after major life events such as marriage, childbirth or adoption, home purchase, or a significant salary increase or career change, to ensure your coverage remains adequate, affordable, and aligned with your current circumstances.Key Takeaway

Life insurance is a tool to protect your family’s financial future. Calculate your needs, choose the right policy type, and review regularly to ensure coverage keeps pace with life and inflation. If you would like a personalised coverage assessment based on your income, debts, and family needs, our advisors can help you calculate a suitable protection amount. Disclaimer This article is for educational purposes only and does not constitute financial advice. Readers should consult a licensed financial advisor for advice specific to their situation.References

- Employees Provident Fund (EPF). (n.d.). EPF death assistance benefit. Retrieved February 25, 2026, from https://www.kwsp.gov.my/en/w/article/epf-death-assistance

- Phillip Capital Management Sdn. Bhd. (2022). Malaysia’s insurance industry: Underpenetration and the call for greater protection. Retrieved February 25, 2026, from https://www.phillipinvest.com.my/malaysias-insurance-industry-underpenetration-and-the-call-for-greater-protection/

- PricewaterhouseCoopers Malaysia. (2023). Revolutionising financial inclusion through digital insurance and takaful. PwC Malaysia. https://www.pwc.com/my/en/assets/publications/2023/20230416-revolutionising-financial-inclusion-through-digital-insurance-and-takaful.pdf

- Social Security Organisation (PERKESO). (n.d.). Social security protection schemes and benefits. Retrieved February 25, 2026, from https://perkeso.gov.my/en/rate-of-contribution/54-social-security-protection/social-security-protection-schemes/

- The Edge Malaysia. (2022, October 17). Cover story: Closing the insurance and family takaful protection gap. Retrieved February 25, 2026, from https://theedgemalaysia.com/article/cover-story-closing-insurance-family-takaful-protection-gap

- Bank Negara Malaysia. (2021). Financial stability and household protection gaps. Retrieved February 25, 2026, from https://www.bnm.gov.my/financial-stability-reports

- Liew, S. Y. (2020). Life insurance planning in Malaysia: Term vs whole life policies and affordability. Malaysian Journal of Financial Planning, 9(2), 45–58.

- Lim, K. H., & Tan, A. L. (2019). Inflation and long-term coverage planning for Malaysian households. Journal of Malaysian Personal Finance, 11(1), 22–37.

- Inland Revenue Board of Malaysia (LHDN). (2024). Tax relief for life insurance premiums. Retrieved February 25, 2026, from https://www.hasil.gov.my/en/tax-relief-life-insurance

- Foo, J., & Chong, M. (2022). Life-stage insurance needs and review strategies in Malaysia. Asia-Pacific Journal of Risk Management, 5(3), 14–28.